Discover our

latest insights

75 Einträge

No insights found.

BRANDL TALOS advises Pride Capital Partners on the acquisition of a minority stake in RUBICON alongside RSM Ebner Stolz

Press release • Venture Capital & Start Ups

Pride Capital Partners, with offices in Amsterdam, Cologne, and Copenhagen, is a hybrid private equity & debt investor focusing on the software and IT industry. With the acquisition of a minority stake in Vienna-based RUBICON Group, Pride completes its first Austrian investment.

ICLG: Gambling Laws and Regulations Austria 2024

Article • Gaming & Entertainment

Austria Chapter covers common issues in gambling laws and regulations – including relevant authorities and legislation, application for a licence, licence restrictions, digital media, enforcement and liability.

BRANDL TALOS advises Telos Impact on EUR 12 million Series A Financing Round of Kern Tec

• Venture Capital & Start Ups

BRANDL TALOS has advised Telos Impact as lead investor on the EUR 12 million Series A financing round of Kern Tec GmbH. The financing round was led by Telos Impact, a leading actor in impact investing, with participation from the PeakBridge Growth II Fund and the European Innovation Council (EIC) Fund.

BRANDL TALOS advises Austrian family office in connection with TDR Capital's investment in Popeyes® UK

Press release • Corporate Law & Transactions

In 2021, BRANDL TALOS has advised long time client "Ring" International Holding AG in connection with its acquisition of the master franchise rights for Popeyes® for the United Kingdom and the establishment of a joint venture with Restaurant Brands International Inc., one of the world's largest quick-service restaurant companies.

BRANDL TALOS advises on sale of ready2order to Zucchetti Group

Press release • Venture Capital & Start Ups

BRANDL TALOS advised as sell-side lead counsel on the sale of ready2order GmbH, the Austrian market leader in cloud-based point-of-sale systems, to the Italian IT market leader Zucchetti.

BRANDL TALOS advises Climentum Capital on €4.5m seed financing round of Fermify

Press release • Corporate Law & Transactions

BRANDL TALOS has advised European ClimateTech fund Climentum Capital as lead investor on the €4.5 million seed financing round of Vienna-based Fermify GmbH.

BRANDL TALOS advises CREANDUM on a USD 20m investment in Prewave

Press release • Corporate Law & Transactions

Prewave extends its Series A by another USD 20m investment led by Creandum.

BRANDL TALOS advises management on sale of Seven Refractories to RHI Magnesita

Press release • Corporate Law & Transactions

BRANDL TALOS advised founder and CEO Erik Zobec as well as other minority management shareholders in the course of the sale of Seven Refractories GmbH's operations in Europe, India and the US to RHI Magnesita. Closing of the approx. EUR 93m transaction is subject to customary conditions precedent and expected in the second half of 2023.

Austria Publishes Draft Law for Implementation of EU Mobility Directive

Article • Corporate Law & Transactions

The Directive (EU) 2019/2121 marks a significant milestone in the development of EU corporate law as it establishes a reliable legal framework for cross-border reorganizations within the EU. Shortly prior to the end of the implementation period, also the Austrian Ministry of Justice published the long-awaited draft law for implementation of the Directive. We have taken a first look at the draft.

Video: 3 questions for Nicholas Aquilina

Video • Gaming & Entertainment

What distinguishes BRANDL TALOS as an employer and why Nicholas enjoys coming to the office in the morning? Find out the answers in our new video!

BRANDL TALOS Turns continues to successfully use Luminance for AI-Powered eDiscovery during in Criminal Investigations

Article • Compliance & Internal Investigations

BRANDL TALOS, one of Austria's leading law firms, has extensive experience with Luminance's AI-powered eDiscovery platformdecided to permanently implement Luminance's AI powered eDiscovery platform in its white-collar crime practice after several successful probationary projects. The software is used One of Austria’s leading law firms, BRANDL TALOS, has today announced its adoption of Luminance’s AI-powered eDiscovery platform to enhance and expedite a range of matters across the firm, including internal investigations and white-collar crime proceedings.

ICLG: Gaming Laws and Regulations Austria 2023

Article • Gaming & Entertainment

Austria Chapter covers common issues in gambling laws and regulations - including relevant authorities and legislation, application for a licence, licence restrictions, digital media, enforcement and liability.

BRANDL TALOS advised KOMPAS on its Series A investment in prewave

Press release • Venture Capital & Start Ups

Prewave just announced its 11m Series A funding round. It was co-led by KOMPAS, a Danish based venture capital firm focusing on businesses that accelerate the digital transformation and industrial automation across the built environment, and Ventech.

BRANDL TALOS expands its litigation team with Anna Katharina Radschek

Press release • Litigation

BRANDL TALOS expands its litigation department and brings on board the experienced lawyer Anna Katharina Radschek (33).

Kiprion completes registration as cryptocurrency service provider with BRANDL TALOS

Press release • Capital Markets

Fintech company Kiprion has been successfully registered with the Austrian Financial Market Authority (FMA) as a "virtual currency service provider" according to FM-GwG.

BRANDL TALOS advises Sportradar on the formation of a joint venture with Ringier AG

Press release • Venture Capital & Start Ups

BRANDL TALOS advised Sportradar Group AG (NASDAQ: SRAD), a leading global provider of sports data and content, on the formation of a joint venture with Ringier AG, a Swiss technology and media company.

BRANDL TALOS advises AVILOO on investment by Invest AG and EIC

Press release • Venture Capital & Start Ups

BRANDL TALOS has advised the Austrian e-tech start-up AVILOO GmbH in the course of an equity investment by Invest Unternehmensbeteiligungs Aktiengesellschaft and its co-investor European Innovation Council Fund (EIC) in the mid-seven-figure range.

Debt eats Equity? The Rise of Venture Debt

Event • Venture Capital & Start Ups

A new form of financing known as "venture debt" is increasingly spilling over from the U.S. to Europe. Although the idea is not new, it could offer founders greater flexibility in their choice of financing - find out more in our video.

BRANDL TALOS advises Fretello on seed financing round

Article • Corporate Law & Transactions

BRANDL TALOS has advised Fretello GmbH on its EUR 3 million seed financing round.

New addition to BRANDL TALOS: Daniel Schmidt joins the corporate & transactional team

Press release • Venture Capital & Start Ups

BRANDL TALOS grows and strengthens its team with Dr. Daniel Schmidt, LL.M. MBA-HSG, (32) adding another highly qualified attorney.

BRANDL TALOS advises Coinpanion in connection with its Seed Extension

Press release • Venture Capital & Start Ups

BRANDL TALOS has advised Austrian FinTech start-up Coinpanion in connection with the expansion of its seed financing round. Following the previously completed seed financing round in August 2021, Coinpanion secured additional funds of EUR 3.7m from, inter alia, renowned investor Wicklow Capital, Bernhard Niesner (busuu), Johannes Braith (storebox), Michael Hurnaus, Wolfgang Reisinger (tractive) and Johann 'Hansi' Hansmann, bringing the total volume of the seed financing round to EUR 5.5m.

BRANDL TALOS advises Sportradar on the acquisition of Vaix

Press release • Corporate Law & Transactions

BRANDL TALOS advised Sportradar Group (NASDAQ: SRAD), a leading global provider of sports data and content, on its acquisition of Vaix Group, a pioneer in developing Artificial Intelligence (AI) solutions specifically designed for the iGaming industry headquartered in London. The transaction completed on 6 April 2022.

BRANDL TALOS advised Indian edtech giant BYJUS'S in connection with its acquisition of GeoGebra

Press release • Corporate Law & Transactions

Think & Learn Private Ltd. (BYJU'S), one of India's most successful startups backed by marquee investors, including Sequoia Capital and Tiger Global, offers an online learning platform that is used by 115 million students. GeoGebra GmbH is an Austrian edtech company that develops and markets a widely-used interactive and collaborative learning tool designed to improve mathematical understanding.

BRANDL TALOS advises lead investor on EUR 18m Series A financing round of Ribbon Biolabs

Press release • Venture Capital & Start Ups

Ribbon Biolabs GmbH, a DNA synthesis company, has completed a EUR 18m Series A financing round led by Hadean Ventures with participation from, amongst others, Lansdowne Partners, Helicase Venture and existing investors IST cube and tecnet equity. A BRANDL TALOS-deal team led by Roman Rericha and Stephan Strass advised the lead investor, Hadean Ventures, on this financing round.

BRANDL TALOS advises lead investors Quadrille and Insight Partners on PlanRadar's USD 69m Series B Financing Round

Press release • Corporate Law & Transactions

PlanRadar, Europe's leading digital field management platform for construction and real estate projects, has completed a USD 69 million financing round co-led by Insight Partners and Quadrille Capital. A BRANDL TALOS-deal team led by Roman Rericha and Stephan Strass advised the lead investors Quadrille Capital and – alongside Willkie Farr & Gallagher – Insight Partners as well as Cavalry Ventures on this financing round, being the third-largest Series B round and the largest-ever for a B2B company in Austria so far.

BRANDL TALOS advised MOSTLY AI Solutions MP GmbH on its Series B financing round

Press release • Venture Capital & Start Ups

MOSTLY AI, which pioneered the creation of AI-generated synthetic data, has raised a $25 Million Series B round. The financing round was led by Molten Ventures (formerly Draper Esprit) with participation from Citi Ventures and the existing investors Earlybird and 42CAP. The BRANDL TALOS-team was led by Roman Rericha and further consisted of Adrian Zuschmann and Julia Strimitzer.

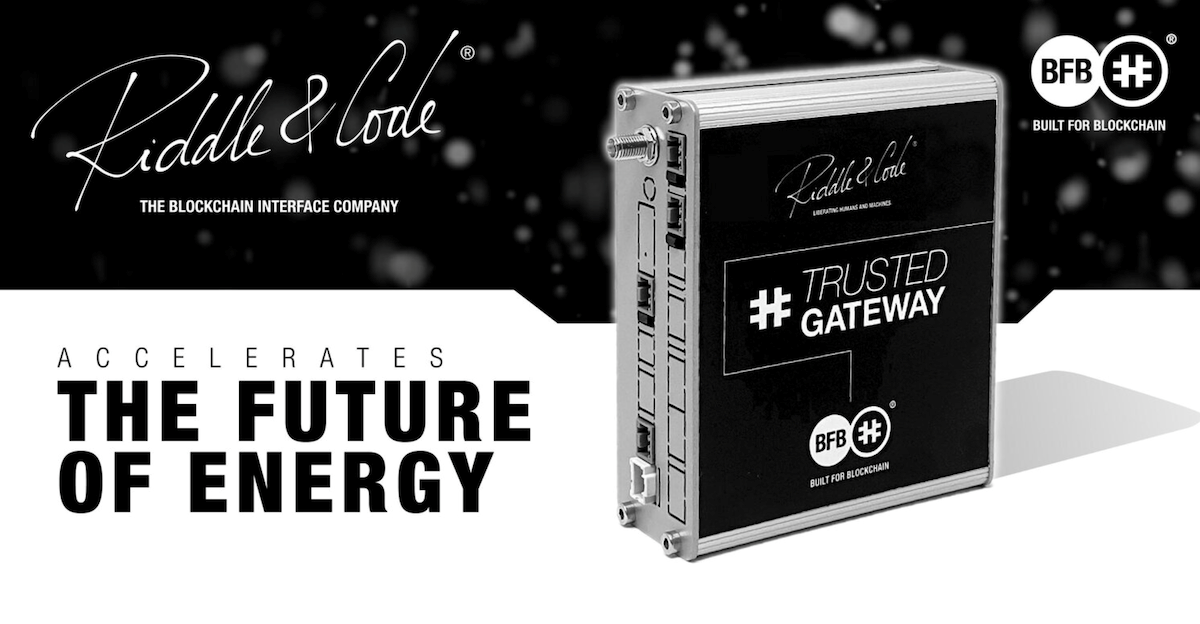

BRANDL TALOS advised RIDDLE&CODE on establishment of joint venture with Wien Energie

Press release • Corporate Law & Transactions

Wien Energie GmbH, one of Austria's largest energy providers, and RIDDLE&CODE, a leading blockchain interface company, have established a joint venture with the objective to accelerate global decarbonisation efforts. Closing of the transaction took place on 9. December 2021. The BRANDL TALOS deal team was led by Thomas Talos and Stephan Strass.

Patrick Mittlböck joins BRANDL TALOS as a lawyer in the Litigation and Gaming & Entertainment Team

Press release • Litigation

Patrick Mittlböck (28), previously Senior Associate, strengthens the team of BRANDL TALOS Partner Nicholas Aquilina in the areas of Litigation and Gaming & Entertainment as of now as an Attorney at Law.

BRANDL TALOS advised AG Capital on set-up of Austrian Growth Capital Fund, alongside Van Campen Liem

Press release • Fund Formation

AG Capital announced its successful first closing of Austrian Growth Capital Fund with capital commitments of EUR 140 million. The fund targets small and medium sized enterprises in Austria and neighbouring countries and shall contribute to close the existing financing gap for growth and buy-out capital in the domestic market. BRANDL TALOS advised AG Capital and C-Quadrat Investment AG, the initiators of the Austrian Growth Capital Fund, on the Austrian law aspects of the implementation of the fund set-up.

ICLG: Austria Gaming Laws and Regulations

Article • Gaming & Entertainment

Covering common issues in gambling laws and regulations - including relevant authorities and legislation, application for a licence restrictions, digital media, enforcement and liability.

BRANDL TALOS has advised TriLite Technologies GmbH on its Series A financing round

Article • Venture Capital & Start Ups

Following a Seed financing round completed in December 2019, TriLite secured EUR 8 mio. in new capital in the course of the Series A.

Career at BRANDL TALOS: Adrian Zuschmann moves up to attorney in the transaction and venture capital team

Press release • Corporate Law & Transactions

Adrian Zuschmann, MSc (30), previously Senior Associate, joins the team of BRANDL TALOS Partner Roman Rericha as a lawyer with immediate effect in the areas of transactions, venture capital and start-ups.

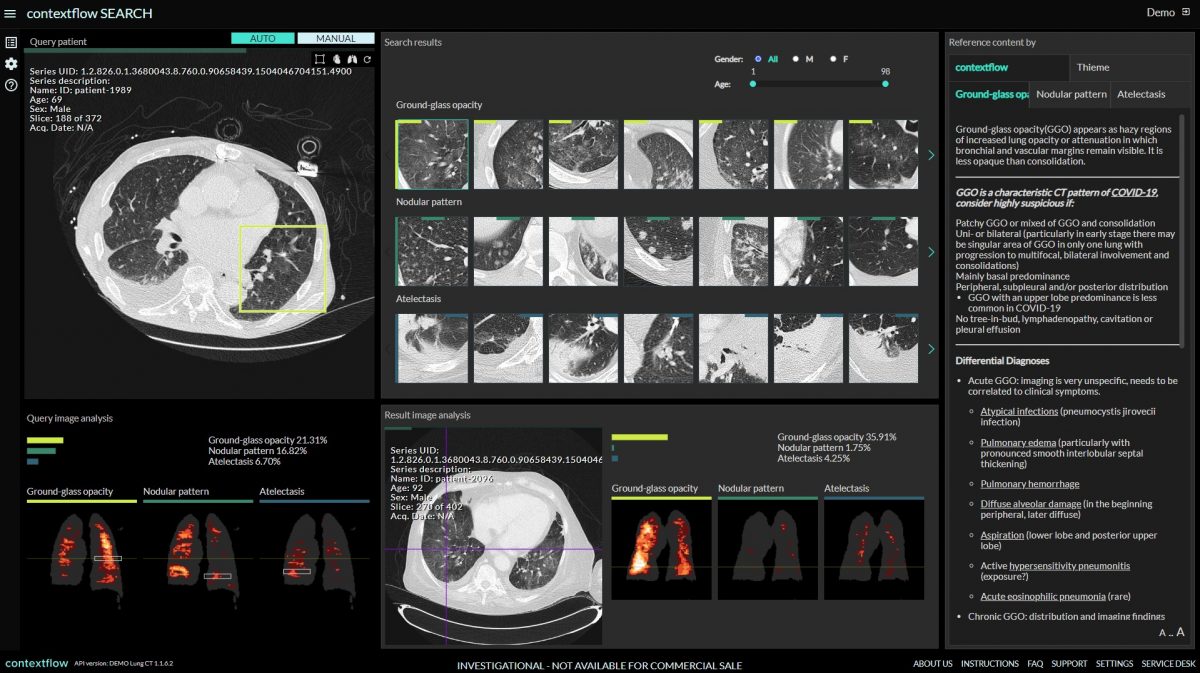

BRANDL TALOS advises contextflow on Second Closing of its Series A financing round

Press release • Venture Capital & Start Ups

Viennese HealthTech start-up contextflow closes 6.7 million euros Series A financing round

BRANDL TALOS advised Sportradar on its NASDAQ-IPO

Press release • Capital Markets

2021 has been an extremely busy year for our long-standing client Sportradar, a leading global provider of sports betting and sports entertainment products and services. Following the acquisitions of Synergy Sports, Fresh Eight and Interact Sport and the conclusion of a long-term deal with the NHL, on all of which BRANDL TALOS advised, Sportradar has now successfully listed its shares on NASDAQ at a valuation of approx. USD 8billion.

BRANDL TALOS advised Capiton on the acquisition of Mauer + Partner GmbH

Press release • Corporate Law & Transactions

German private equity firm Capiton, advised by Lupp + Partner (Kerstin Kopp) as lead transaction counsel, acquires a majority stake in German Kutterer Mauer AG, a global manufacturer of closures and closure solutions.

BRANDL TALOS advises AC Immune on the Acquisition of Parkinson's Disease Vaccine Candidate

• Corporate Law & Transactions

Alongside Bär & Karrer, BRANDL TALOS advises AC Immune on the Strategic Acquisition of Industry-leading Parkinson's Disease Vaccine Candidate and Equity Investment

BRANDL TALOS advised Sportradar on 10-year global partnership with NHL

Press release • Corporate Law & Transactions

Sportradar, a leading global provider of sports betting and sports entertainment products and services announced a 10-year global partnership with the National Hockey League (NHL).

BRANDL TALOS advised shareholders of Allcyte on sale to Exscientia

Press release • Corporate Law & Transactions

Exscientia, a leading clinical stage pharmatech company, has entered into a binding agreement to acquire Allcyte, a leader in artificial intelligence (AI) based precision medicine. The transaction is subject to customary regulatory approvals.

BRANDL TALOS advises contextflow on Series A financing round

Press release • Venture Capital & Start Ups

contextflow raises seven-digit investment in Series A financing round.

Video: Students at BRANDL TALOS - Start a career as a student

Video

At Brandl Talos, we believe in learning by doing, in growing with tasks and in getting the right guidance to do so. In our student program, we give the aspiring next generation lawyers the opportunity to actively contribute to our team's success from the very beginning, to learn in practice and to receive the support that will help them grow as individuals.

BRANDL TALOS advises RIDDLE&CODE on registration proceedings before the FMA

Press release • Banking, Insurance and Securities Regulation Law

Fintech company RIDDLE&CODE FinTech Solutions has been successfully authorized by the Austrian Financial Market Authority (FMA) as a "virtual currency service provider". This makes the company one of the first to receive the corresponding authorization in Austria.

BRANDL TALOS advises Sportradar on the Acquisition of InteractSport

Press release • Corporate Law & Transactions

BRANDL TALOS advised Sportradar Group, a leading global provider of sports data intelligence and sport entertainment solutions, on its acquisition of InteractSport Group, a sports data and technology company based in Australia and England with partnerships across a range of leading sports organisations with a particular expertise in cricket. The acquisition is subject to regulatory approvals and expected to close in Q2/2021.

Alexander Stücklberger strengthens the white-collar crime team at BRANDL TALOS as an attorney at law

Press release • Compliance & Internal Investigations

Alexander Stücklberger (28), who has been with BRANDL TALOS for many years, joins partner Christopher Schrank's team as an attorney at law in the areas of white-collar crime and compliance.

BRANDL TALOS advises International VC Syndicate on Investment in Allcyte

Press release • Corporate Law & Transactions

BRANDL TALOS advised an international syndicate of venture capital funds, including 42CAP (alongside SMP – Frederik Gärtner) and Amino Collective (both Germany), PUSH Ventures (Austria), Air Street Capital (UK) and VP Venture Partners (Switzerland), on their investment in Allcyte GmbH, an Austrian biotech firm focused on functional drug testing in primary human material.

BRANDL TALOS advises Austrian family office in its investment in Popeyes UK

Press release • Corporate Law & Transactions

Following its acquisition of the Burger King master franchise in Scandinavia, "Ring" International Holding AG has reached an agreement with PLK Europe GmbH an affiliate of Restaurant Brands International Inc. ("RBI"), to become the UK master franchisee of Popeyes® with exclusive rights to the brand in the UK.

BRANDL TALOS advises Sportradar Group on the Acquisition of Synergy Sports

Press release • Corporate Law & Transactions

Alongside Latham Watkins (USA), BRANDL TALOS advised its long-standing client Sportradar Group, a global leader of sports data and content delivery, on its acquisition of Synergy Sports, a pioneer in automated sports technology solutions and the market leader in data and video analytics in the US college and professional sports space.

BRANDL TALOS advises Sportradar Group on the Acquisition of Fresh Eight

Press release • Corporate Law & Transactions

BRANDL TALOS advised Sportradar Group, a global leader of sports data and content delivery, on its acquisition of Fresh Eight, a UK-based operator of a personalized messaging platform.

BRANDL TALOS advises btov on investment in data analytics startup Visplore

Press release • Nährboden - Our Start-up Program

Vienna-based startup Visplore has received €1 million in funding from btov Partners' Industrial Technologies fund for its innovative graphical analysis software.

Chambers Global 2021: Multiple awards for BRANDL TALOS

Article • Gaming & Entertainment

The international legal directory Chambers Global has once again acknowledged the expertise and track record of our Gaming, Corporate/M&A and Litigation practice groups at BRANDL TALOS.

Video: Our team members have their say - What does it mean to be open-minded?

Video

We are open-minded: And not only on a personal level, but also on a substantive level. We are also open to the unknown and like to discover new ways to develop the best possible solutions for our clients.

Video: Our team members have their say - What does it mean to be agile?

Video

We are AGIL: For us, this means having our finger on the pulse of the time, proactively driving projects and cases forward, and - wherever possible - thinking "out of the box". Thanks to our numerous teams of experts, we are able to serve our clients quickly and efficiently at any time, responding to the call for specialization that has been unbroken for years.

Video: Our team members have their say - What does it mean to be focussed?

Video

We are FOCUSED: We always have a clear goal in mind, to provide the best possible legal advice. To support our clients in a targeted manner in making the best decisions for the success of their business - that is our mission. And this is what we live day by day in our law firm.

We proudly present: Our new Corporate Design

After twenty years of blue, we have decided to change our corporate design to better reflect our firm’s identity going forward.

The only current short commentary on the KMG!

Book • Banking, Insurance and Securities Regulation Law

The legislature has thoroughly revised the KMG in 2019 - due to the Prospectus Regulation. Raphael Toman and Andreas Frössel prepare the relevant issues together with a strong team of authors in their book.

Managing Director Liability - Contracts Shortening the Statute of Limitations inadmissible

• White-Collar Crime

According to the law, claims for compensation by the GmbH against "its" managing directors become time-barred within five years. In practice, however, shorter limitation periods are often agreed. This is to encourage managing directors to make entrepreneurial decisions by not leaving them in the dark for too long with regard to possible liability. According to a recent decision of the Austrian Supreme Court, however, such reductions are invalid.

Brandl Talos and SMP advise S.I.E. AG on the acquisition of a majority stake of EMGR GmbH

Press release • Corporate Law & Transactions

Vienna, 18 December 2020 - System Industrie Electronic Holding AG acquires 70.1% of Elektromotorenwerk Grünhain GmbH, a developer and manufacturer of actuators and actuator components for a wide range of industrial applications.

At which point are there penal consequences for auditors? (GER)

Article • White-Collar Crime

New challenges: E-sports as sport or as gimmick?

Article • Gaming & Entertainment

E-sports, i.e. competitive video and computer games, have long ceased to be a marginal phenomenon in Austria. Nevertheless, e-sports are still in a legal gray area. But the wait for clear legal regulations may be over: The Sports Committee in the National Council has taken on the task of creating a legal framework for e-sports.

European Court of Justice contradicts EU Commission and confirms: CBD is not an addictive substance

Article • Nährboden - Our Start-up Program

Landmark ECJ decision opens the door to new business and investment opportunities in the CBD industry.

Safeguarding in the digital age (GER)

Article • White-Collar Crime

Whistleblowers: a blessing for companies? (GER)

Article • Compliance & Internal Investigations

The Virtual Currency Regulation Review (third edition)

Book • Capital Markets

ICLG Gambling 2021, Austria Chapter

Book • Gaming & Entertainment

Brandl Talos advises biotech start-up Sarcura on EUR 2.5 million seed financing round

• Venture Capital & Start Ups

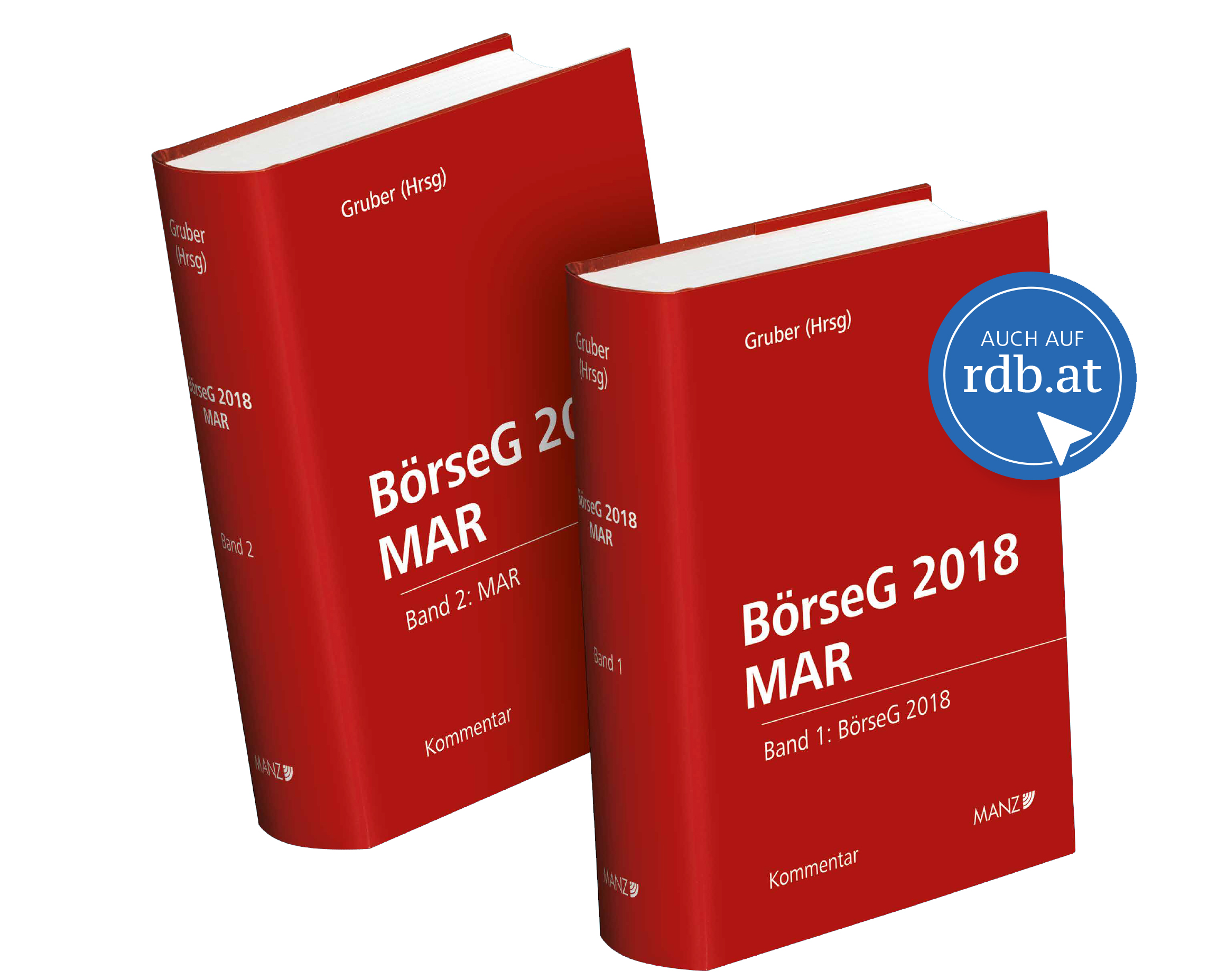

BörseG 2018/MAR - the flagship of Austrian literature on the new Stock Exchange Act (GER)

Book • Capital Markets

The new Manz commentary "BörseG 2018/MAR" is the flagship of Austrian literature on the new Stock Exchange Act and the Market Abuse Regulation. In it, Christopher Schrank and Alexander Stücklberger comment on the judicial criminal regulations for insider trading and market manipulation, which are particularly important for practice, as well as the special regulations regarding criminal proceedings.

"Cage the beast": virtual currencies in the CRR regime (GER)

Article • Capital Markets

WiEReG compliance package simplifies KYC processes

Article • Compliance & Internal Investigations

As of November 10, 2020, the legislative changes surrounding the WiEReG compliance package will come into effect. Companies will then be able to submit their KYC documents to the register of beneficial owners.

Brandl Talos advises aws Gründerfonds on its investment in the Viennese start-up Rendity

Article • Nährboden - Our Start-up Program

Advising on the acquisition of Burger King in Scandinavia

Article • Corporate Law & Transactions

Vienna, October 28, 2020 - "Ring" International Holding AG ("Ring") acquires Burger King's franchise business in Norway, Sweden and Denmark from Umoe Restaurant AS.

Guide for start-ups

Book • Nährboden - Our Start-up Program

The criminal liability of the compliance officer (GER)

Article • Compliance & Internal Investigations

Securing smartphones with fingerprint or Face ID (GER)

Article • White-Collar Crime

Brandl & Talos advises shareholders on the sale of Themis to Merck Sharp Dohme

• Corporate Law & Transactions

Vienna, May 27, 2020 - With this acquisition, Merck Sharp Dohme (MSD) secures, among others, the COVID-19 vaccine developed by Austrian company Themis, which will be combined with an MSD vaccine platform to contribute to the global fight against coronavirus.

Requirements for Reliability in Sports Betting Law: A Comparative Legal Analysis (GER)

Article • Gaming & Entertainment

Market manipulation through statements, interviews and tweets

Article • White-Collar Crime